Doug Carey for Seeking Alpha writes: Many investors who are fans of mortgage REITs are pointing to the

possibility of a near-perfect scenario: The Federal Reserve stops buying

mortgage-backed securities (which would mean higher yields on

mortgage-backed securities) but keeps short-term rates extremely low. This

would be the sweet spot for mortgage REITs because they would be able

to continue to borrow money cheaply, but can then invest in higher

yielding mortgage-backed securities. In other words, their spread would

increase and thus their profitability.

Even though many mortgage

REITs pay a nice dividend, investors are sometimes surprised by the

hefty tax bill. REITs are taxed at ordinary income tax rates if they are

in taxable accounts, which takes a big bite out of the total return for

many. But there is a way to get around this tax bill if an investor has

capital losses he can use. I call this strategy dividends to capital

gains conversion.

The idea is this: By taking dividends in the

form of capital gains, and then offsetting those gains with capital

losses you may have, you can pay an effective tax rate of 0%. Compare

this to paying either the 15% rate for qualified dividends (for most

people) or your top marginal income tax rate on REIT investments.

So

how does one go about converting dividends to capital gains? It takes

some monitoring, but it could very well be worth your time. First let's

define the ex-dividend date for a stock:

The ex-dividend date is

the day on which all shares bought and sold no longer come attached

with the right to be paid the most recently declared dividend. This is

an important date for any company that has many stockholders, including

those who trade on exchanges, as it makes reconciliation of who is to be

paid the dividend easier. It is just as important for investors,

however, since you must own a stock before the ex-dividend date in order to receive the next scheduled dividend.

If

an investor buys the stock on the ex-dividend date or after, he is not

entitled to the next dividend. This also means that if an investor sells

the day before the ex-dividend date, he is not entitled to the next

dividend.

Given this, an investor can buy a stock the day of the

ex-dividend date and sell the day before the next ex-dividend date, and

be assured that he will never receive a dividend. Some might be saying

what a horrible deal! But Mr. Market is no dummy. Those who buy on the

ex-dividend date and sell the day before the next one will benefit from

the stock price climbing by the amount of the dividend during this time.

If you ever notice why a stock's price drops the of the ex-dividend

date, this is because those buying it on that day will not receive the

next dividend. In fact, the price drops by the amount of the next

dividend. Conversely, the stock price will begin climbing the day after

the ex-dividend date and will eventually rise by the amount of the

dividend. Of course, the price will fluctuate due to other variables,

but the amount of the next dividend is always embedded in the price.

Hopefully this all makes sense because for stocks with high dividend

yields, as this strategy could provide a huge gain for investors. Let's

take a look at how this strategy might be used with Annaly Capital (NLY), which has a dividend yield today of 11.5%.

Every

quarter if I buy NLY on the ex-dividend date and then sell it the day

before the next ex-dividend date I pay no taxes whatsoever on this

dividend, yet receive all of the dividend yield in the form of capital

gains. I avoid taxes by offsetting the gains with capital losses. This

is a huge benefit to me because NLY is a REIT and investors must pay the

full income tax rate on any dividends that are paid.

Let's look

at an example using NLY where an investor buys 5,000 shares. The

combined marginal federal and state tax rate for the investor is 33%.

The investor is able to offset all capital gains with capital losses and

pays $8 per trade. I ran the following using our publicly available

calculator called Minimize Taxes by Trading Dividends for Capital Gains and readers are free to run their own scenarios as well.

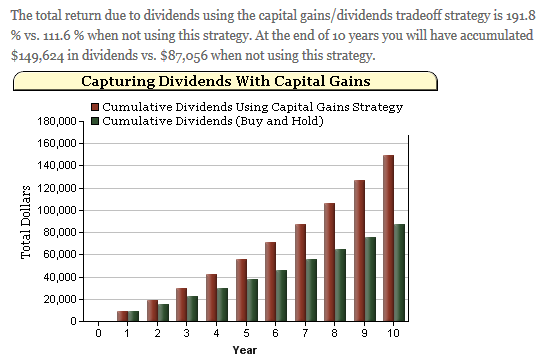

I will have accumulated nearly $63,000 more over 10 years using this

strategy. That is a cumulative return that is 80% higher than if I just

collected the dividend. I can also adjust the amount of the capital

gains that I can offset. Let's say I can offset 50% of the gains with

capital losses. It is still worth it because this strategy delivers a

49% higher return than not using the capital gains conversion strategy.

Other REITs where this strategy would work well are American Capital Agency Corp. (AGNC), New York Mortgage Trust (NYMT), Dynex Capital (DX), Anworth Mortgage Asset Corp (ANH), and Hatteras Financial (HTS).

| Ticker | Dividend Yield |

| AGNC | 15.7% |

| NYMT | 15.0% |

| DX | 11.2% |

| ANH | 9.9% |

| HTS | 10.3% |

Because

of the monitoring involved and the trading costs, this idea is best

suited for those stocks with relatively high dividends. In the example

above, if the dividend yield were below 2%, this strategy does not pay

off any more. But for REITs and other high yielding stocks, especially

those where dividends are taxed at your income tax rate, this strategy

will be a sure-fire winner.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in NLY, AGNC over the next 72 hours. I

wrote this article myself, and it expresses my own opinions. I am not

receiving compensation for it (other than from Seeking Alpha). I have no

business relationship with any company whose stock is mentioned in this

article.

0 comments:

Post a Comment