When you are self-employed, it typically means you work for yourself, as an independent contractor, or own your own business. Here are six key points the IRS would like you to know about self-employment and self-employment taxes:

1. Self-employment income can include pay that you receive for part-time work you do out of your home. This could include income you earn in addition to your regular job.

2. Self-employed individuals file a Schedule C, Profit or Loss from Business, or Schedule C-EZ, Net Profit from Business, with their Form 1040.

3. If you are self-employed, you generally have to pay self-employment tax as well as income tax. Self-employment tax includes Social Security and Medicare taxes. You figure this tax using Schedule SE, Self-Employment Tax.

4. If you are self-employed you may have to make estimated tax payments. People typically make estimated tax payments to pay taxes on income that is not subject to withholding. If you do not make estimated tax payments, you may have to pay a penalty when you file your income tax return. The underpayment of estimated tax penalty applies if you do not pay enough taxes during the year.

5. When you file your tax return, you can deduct some business expenses for the costs you paid to run your trade or business. You can deduct most business expenses in full, but some costs must be ’capitalized.’ This means you can deduct a portion of the expense each year over a period of years.

6. You may deduct only the costs that are both ordinary and necessary. An ordinary expense is one that is common and accepted in your industry. A necessary expense is one that is helpful and appropriate for your trade or business.

For more information, visit the Small Business and Self-Employed Tax Center on the IRS website. There are three IRS publications that will also help you. See Publications 334, Tax Guide for Small Business; 535, Business Expenses and 505, Tax Withholding and Estimated Tax. All tax forms and publications are available on IRS.gov or by calling 800-TAX-FORM (800-829-3676).

Karin Price Mueller/The Star-Ledgerfor NJ.com writes: Q. With a dividend reinvestment plan, or DRIP, if there is a fee charged for the service, can the fee be deducted on my income tax return?

-- Drippy investor

Answer. The Brain always loves to hear when people are taking part in regular investment plans. That's the best way to build wealth over time.

DRIPs are an excellent way to create an automated savings plan, said Michael Maye, a certified financial planner and certified public accountant with MJM Financial in Berkeley Heights.

Before getting to your tax question, Maye recommends you consider an investment firm that offers a cost-free dividend reinvestment program. For example, he said, TD Ameritrade account holders who enroll in TD's DRIP program do not pay a fee to reinvest their dividends.

In terms of your question, it comes down to what type of costs are being incurred in the DRIP program, he said.

"If the cost is a commission, it is added to the investment's cost basis. In this case, the tax benefit is not realized till the investment is ultimately sold," he said. "Any non-commission-related costs or fees associated with a DRIP program would qualify as Schedule A miscellaneous itemized deductions subject to the 2 percent of AGI limitation."

AGI is adjusted gross income, and you need to know how to make that calculation.

"First, you compute your total of all expenses that fall into miscellaneous deduction categories," said Gail Rosen, a Martinsville-based certified public accountant. "This amount is deductible as an itemized deduction but only -- and to the extent -- it is greater than 2 percent of your AGI."

Rosen said that because it's an itemized deduction, it can only be claimed if you itemize your deductions and don't claim the standard deduction. Other miscellaneous itemized deductions to consider here include tax preparation costs, employment-related expenses and investment expenses, she said. One final caveat, Rosen said, is that the deduction for miscellaneous itemized deductions is not allowable for the alternative minimum tax (AMT). And one other consideration. While DRIPs are a great way to save automatically, there is no real thing as an auto-pilot investment program. You need to always be vigilant and consider how any automatic investment is impacting your overall financial picture. "When using a DRIP strategy make sure and diversify to avoid being over concentrated in one stock," Maye said. Good advice.

Robert D. Flach for MainStreet.com writes: A “point” is a percentage fee charged to obtain a mortgage. One point on a $100,000 mortgage is $1,000. Points, aka Loan Origination Fee or Loan Discount, are usually reported on Lines 801-803 on the Closing Statement. Points can be deducted as interest on Schedule A.

Points are usually “amortized” over the life of the loan. Points on a 30-year mortgage are deducted over 360 months. But you can deduct the total number of points paid in full in the year paid on a mortgage used to purchase, build or substantially improve your principal residence.

To deduct the points in full in the year of purchase, the amount of money paid at closing, including any seller-paid points and the initial down payment or deposit, must at least equal the number of points charged. If the points on a $300,000 mortgage are $6,000 and you had made a $1,000 deposit and paid $25,000 at closing, the $6,000 is fully deductible.

Points paid to refinance your principal residence or to purchase or refinance a vacation home or investment property must be amortized over the life of the mortgage. However, if you refinance a mortgage on your principal residence in order to get additional money to improve the residence substantially, you can deduct in full the points paid on the funds used for the improvements.

If you pay-off a mortgage on which you have been amortizing points - you sell the property or refinance the mortgage with a new lender - you can deduct the amount of “unamortized” points on that mortgage in full in the year of the pay-off. If you paid $3,600 in points on a 30-year mortgage to purchase a vacation home and have deducted a total of $540 in points on prior years’ tax returns, then when you sell the home, you can deduct $3,060 in points on Schedule A.

But this doesn’t work if you refinance the mortgage with the same lender. You purchased the vacation home with a mortgage from Chase. You refinance the mortgage with Chase to get a lower interest rate and to reduce the term to 15 years. There are no points on the refinance. Because you refinanced with the same lender, the remaining $3,060 in unamortized points must continue to be amortized over the 180 month term of the new loan.

Swizznet, a premier QuickBooks hosting and online accounting solution provider, is expanding its offerings by being the first to offer cloud-hosted QuickBooks Point of Sale 2013 for both single- and multi-lane environments. The multi-lane capability allows retailers with more than one cash register to utilize the service -- whether it's at multiple locations or multiple points of sale within one store. With multi-lane, retailers benefit from instant access to financial data that gives a complete picture of all of their sales and inventory from all points of sale. Swizznet, the most technically sophisticated of online accounting providers, collaborated with Intuit for months on cloud-enabling multi-lane.

"Swizznet is excited to be first to offer cloud-hosted Point of Sale for multi-lane environments," said Kristin Callan, COO, Swizznet. "Our customers have been requesting this capability for some time and we are confident that the time we've taken to perfect this single- and multi- lane hosted-solution has resulted in one of the most reliable and robust online accounting/POS offerings to date. We're very proud to again prove our technical leadership by delivering a hosted service that was previously impossible."

QuickBooks Point of Sale 2013 provides the payment processing, detailed sales and inventory reports and customer shopping histories needed to help the nation's 2.8 million small businesses grow. This most recent version includes Intuit's GoPayment mobile feature that allows a business to accept credit and debit cards on a mobile phone or tablet, with all mobile sales and inventory information syncing with QuickBooks to keep records accurate and up-to-date.

Businesses choosing Swizznet's cloud hosted version of QuickBooks Point of Sale do so for the same reason they choose Swizznet's hosted QuickBooks -- it allows them to focus on growing their business and not on IT. By utilizing Swizznet's solutions, business owners and accountants don't have to become IT experts. Swizznet and its US-based technical support and engineering teams assist with implementation and are on call for any need that may arise. Additionally, customers cite the anywhere/anytime access to their accounting software and financial systems that hosted solutions provide as a key benefit, allowing them to manage their business wherever they are, anytime of the day or night.

From TheBizTV. The alternative minimum tax (AMT) was invented by an imaginative group of legislators attempting to capture wealthy Americans, who through artful and tactical tax planning were legally paying little to no tax. But the AMT was never inflation-adjusted and as inflation increased earnings many middle class tax payers were being trapped in a rich man’s progressive tax. Finally, after decades of middle class entrapment, the AMT was recently changed and is adjusted for inflation going forward. Another area of attention is long term capital gains and losses. Many skilled investors as well as accountants try to offset capital gains against capital losses at the end of the year to reduce exposure to capital gains taxation. But sometimes capital losses exceed gains and the IRS limits those losses to $3,000 a year until they are recovered. Steve and Ken bring you up to speed on the AMT, capital gains and losses with strategies that can help you minimize your tax liability.

The AMT, Capital Gains & Losses (Income Tax Planning Series for 2013) from The BIZ on Vimeo.

Ed Slott for Financial-Planning.com writes: Alittle-noticed provision of the big New Year's tax deal could have significant impact on some of your clients. New rules for in-plan Roth 401(k) conversions have opened up some interesting new planning possibilities - and although the conversions come with a few pitfalls, some clients will find them to be a valuable option.

In-plan Roth conversions were first introduced into law back in 2010, as part of the Small Business Jobs Act. The idea was to allow plan participants an opportunity to move money from the traditional side of their company plan, such as a 401(k), to a Roth 401(k) within the plan. Plans that can offer a Roth option include 401(k), 403(b) and governmental 457(b) plans. (The federal government's thrift savings plan also offers a Roth option.)

When that act was introduced, the rules did not allow clients to make an in-plan Roth conversion unless they were eligible to take a distribution of their plan funds - for the most part, restricting it to workers who had either left the company or were older than 591/2. In essence, this meant that nearly every client eligible to make an in-plan Roth conversion could also make an ordinary Roth IRA conversion, minimizing the impact of the law. The new tax deal (known formally as the American Taxpayer Relief Act) modifies the original 2010 rules by allowing clients to make in-plan conversions even if they are not eligible to take a distribution from the plan. That broadens the impact considerably: Many more clients will now be able to make this type of conversion. Lawmakers included the in-plan conversion rule changes as a revenue raiser. Many have already questioned its status as a true revenue raiser and believe adding this option will cost the government in the long run. WHO'S ELIGIBLE? Just because the new law makes it easier for clients to make in-plan conversions doesn't mean all clients with 401(k)s or similar plans will be able to make them. Many plans don't even offer a Roth component. And not all plans with Roth options allow in-plan conversions; both the Small Business Jobs Act and the fiscal cliff deal left them at the plan's discretion. But for those clients who now have the opportunity to make in-plan conversions, you'll need to evaluate two key issues: * Does a conversion of any type make sense? * If so, is an in-plan conversion a better option than a Roth IRA conversion?

KEY FACTORS Any conversion should be considered carefully. The resulting income could impact the client's tax rate, deductions, credits, phaseouts, AMT, exposure to the health care surtaxes and financial aid for which they or their children are eligible. When determining whether a client should convert, advisors should continue to focus on three big questions. First, ask clients when they will need the money. Generally, if a client will need the money soon, a Roth conversion does not make sense. (Since these funds are in a plan, this question may be moot; if your clients intend to keep working, they may not have access to the funds for several years.) The next question to address is where a client would get the money to pay the tax bill on the in-plan conversion. If the client intends on using assets from an existing retirement account to help cover the taxes, the conversion almost never makes sense. The final and critical question for clients is this: What do you think your future tax rate will be? For clients who believe they will be in a lower tax bracket in the future, a Roth conversion now probably does not make sense. But if the client believes the future tax rate will be higher, it's worth considering a Roth conversion now. Remember, just because the latest tax rates are being called "permanent" does not mean Congress can't pass a new law increasing them down the road.

IN-PLAN PITFALLS If a Roth conversion is the right move for your clients, the next step is to determine whether an in-plan conversion is right for your client. Perhaps the biggest downside to an in-plan conversion is that there is no way to recharacterize, or undo, the conversion. This creates a number of complications and planning concerns. For starters, the ability to pay the resulting tax bill becomes far more important on an in-plan conversion. If clients have unexpected difficulties paying the tax on a Roth IRA conversion, they have until Oct. 15 of the year following the year of conversion to recharacterize the move, eliminating the tax bill. The decision to make an in-plan conversion, however, is irrevocable - as is the resulting tax bill. Therefore, be sure you have taken into consideration such possibilities as a client's loss of employment or disability prior to recommending an in-plan conversion. If your clients can't pay the tax bill, they will be in deep trouble. Even if clients have more than enough money to pay the tax bill, the lack of a recharacterization option creates other issues. What happens, for instance, if a client's account value drops precipitously after converting? While you would obviously try to avoid this in any account, the consequences would be far worse after an in-plan conversion. At least with a Roth IRA conversion your client could recharacterize to avoid paying tax on lost value; with the in-plan conversion, however, your client will be stuck paying tax on the value initially converted. In-plan conversions also limit certain planning strategies, such as the cherry-picking of losing accounts. While the tax code does not allow clients to recharacterize specific (poor-performing) investments within a Roth IRA account, investors can choose the Roth IRA accounts they would like to recharacterize. This subtle difference offers the strategy of converting to multiple accounts so that you can cherry-pick winning accounts and recharacterize other accounts that contain losing investments.

OTHER DISTINCTIONS The lack of a recharacterization option is probably the biggest potential drawback of an in-plan conversion, but there are other differences to be aware of. One reason some clients prefer Roth IRAs over traditional IRAs is that Roth IRAs have no required minimum distributions - but the same cannot be said for Roth 401(k)s and other in-plan Roth accounts. Once clients turn 701/2, they must take these required distributions - unless, in some cases, if they are still working. The distributions can be sidestepped easily, however, by rolling the Roth 401(k) into a Roth IRA one year before they are required. Other complications to watch for include separate five-year clocks for Roth accounts maintained in different plans, as well as in-plan Roths' complicated pro rata distributions to balance taxable and nontaxable withdrawals - a difference from the ordering rules applicable to Roth IRA distributions.

WHO BENEFITS? Despite these potential pitfalls, in-plan Roth conversions will indeed make sense for some clients. Those likely to benefit most from the new changes are young clients who plan on remaining with their employers for the foreseeable future. Prior to the changes in the fiscal cliff tax deal, these clients likely had little or no opportunity to make in-plan Roth conversions: The ability to take a distribution of plan funds is generally limited for clients who are still working for the plan sponsor and are younger than 591/2. Under the new rules, however, these clients may be able to convert their plan assets immediately. Other clients who might benefit from in-plan Roth conversions are: * Clients concerned about creditor protection who live in a state with poor protection for Roth IRAs. * Clients who wish to use Roth plan funds to purchase life insurance, which is a prohibited investment in Roth IRAs. * Clients who want to use a loan to access their Roth funds (a prohibited transaction in a Roth IRA). Other clients who want to mitigate some of the pitfalls of the in-plan Roth conversions may choose to do partial conversions over a number of years, rather than converting an entire employer plan account balance. This would help allay concerns about the lack of a recharacterization option and help reduce the impact of higher income on their tax returns.

Yardena Arar for PC World writes: The race is on. As procrastinators gather their W-2 forms and receipts, small-fry tax sites and apps battle with three full-fledged software programs—H&R Block at Home, TaxAct, and TurboTax—for your last-minute filing business. Choosing the right site, program, or app is a decision you shouldn’t make in haste, because you don’t want to find yourself lacking one or more of the forms you need, or paying more to file than you need to.

This rundown of the major Web, mobile, and software options will help you decide which option best suits your tax situation. Users with relatively modest income and tax situations might be eligible for free Web-based tax preparation and e-filing. The small-fry websites are competent—but they’re not necessarily cheaper than the Big Three programs, let alone as polished. Of the three leading packages, TurboTax is the leader (and the most expensive), H&R Block can brag about its small army of tax pros, and TaxAct is the most affordable full-fledged option. A few mobile apps for smartphones and tablets are available, but they assume that your tax-paying requirements are pretty straightforward.

One more note: Pay special attention to what it costs to prepare your return using the software, and then what it costs to file the return electronically, as opposed to printing and mailing the return. E-filing fees can get especially high for state returns.

Who gets free Web-based prep and e-filing

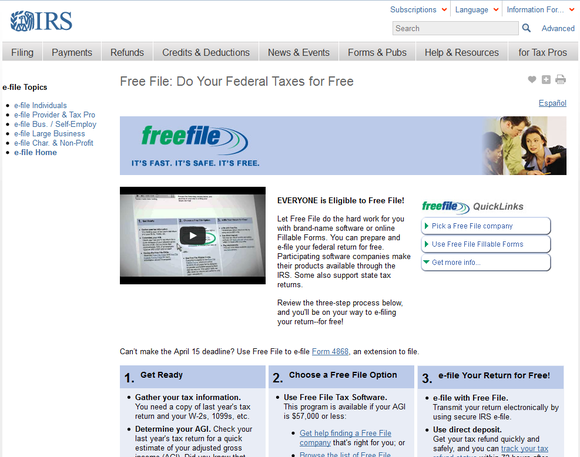

Good news for many taxpayers with simpler returns: You might be able to prepare and file your federal taxes online for free. To qualify, your adjusted gross income (income after deductions) must be $57,000 or less, and you can’t have Schedule C self-employment or business income, complex investment income, or deductions beyond dependents and perhaps a home mortgage. Go through the IRS’s Free File page (you can’t get to the free options through the vendors’ webpages) to find participating vendors and their requirements—age range or military service, for example. Even if you don’t qualify for FreeFile, you can use the list as a reference guide for Web-based tax prep.

MELISSA RIOFRIOFilers with modest income and fairly simple tax situations can file for free through the IRS.

FreeFile covers only your federal return. Sites charge extra—usually around $30—for state returns. Generally, the less expensive the federal return, the more you’ll wind up paying for state tax prep and e-filing.

No matter how high your income, if you’re just looking for a way to fill out and file tax forms online using only the instructions provided by the feds, head to the Free File Fillable Formssection of the Free File site. You’ll find a list of supported forms and known issues to check out before you get started.

Taxbrain, TaxSlayer, and other Web options

Web-based services overtook desktop software in popularity several years ago, and it’s easy to see why. You don’t have to deal with installation or update hassles, and the services offer easy access from any standard browser. Most of the services on the FreeFile list support only Web-based tax prep.

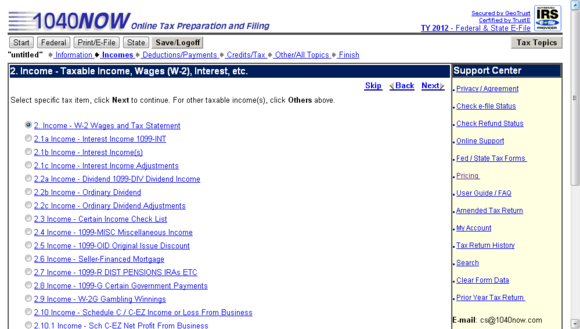

YARDENA ARARSome of the small-fry websites are downright geeky, like 1040Now’s outline-based interface.

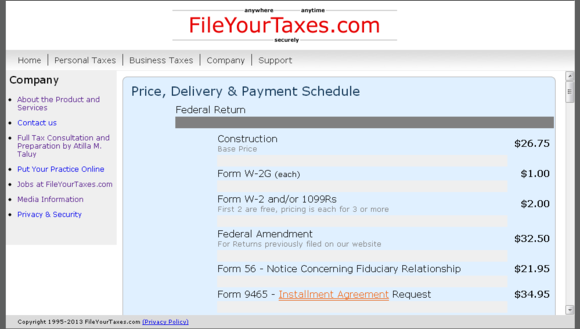

A dozen Web-based tax services, including heavily promoted ones such as eSmart Tax(formerly CompleteTax), Taxbrain, and TaxSlayer, compete with the Big Three for online filing business. All of them make it possible to file a tax return online, but they can’t match the big names in several key ways: handsome user interfaces, convenient features such as a data-import capability, and assistance from real tax pros. Some of the smaller sites are downright geeky: 1040Now, for example, presents forms in an outline format, as opposed to the Q&A, interview-style approach of more-polished services. Others provide little more than IRS form questions with basic definitions that you can get in the IRS instructions.

YARDENA ARARThe smaller players typically don’t cost less than more full-featured services.

More important, the smaller players don’t necessarily cost less than the more full-featured services. TaxBrain, for instance, charges $15 to $70 for its online federal tax prep, depending on the complexity of your tax situation. State preparation and e-filing, however, add another $30 to the bill, so TaxBrain's total cost isn’t much lower than that of H&R Block at Home products.

Deciding among TurboTax, H&R Block, and TaxAct

The two 900-pound gorillas of the tax-prep game are Intuit’s TurboTax and H&R Block.TaxAct from 2nd Story Software caters to the budget crowd.

TurboTax, H&R Block at Home, and TaxAct all offer desktop software on media or as a download. Versions increase in price along with the complexity of your tax situation, and the sites explain the differences well. The most complex packages cover self-employed people or small business owners who file Schedule C for sole-proprietor businesses.

One major reason to stick with desktop software is if you want to prepare multiple returns: A Web-based service charges for creating a single return, usually with e-filing charges included. Desktop H&R Block or TurboTax software lets you create as many returns as you wish, and you may e-file up to five returns. TaxAct’s desktop software is available for $13 with electronic filing for one return and $8 for each additional e-file—or you can pay $20 up front for up to five e-files.

Things get more complicated if you also want to create and e-file state returns. Both H&R Block and TurboTax include software for a state return in all but their most basic download packages, but they charge extra for electronic filing of state returns—which is especially bad news if you have income in more than one state.

TurboTax leads in features—and expense

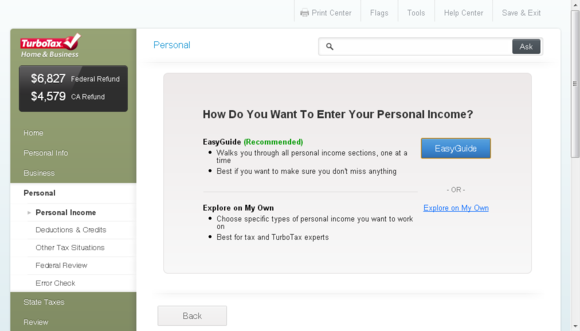

TurboTax costs more than the others, but it offers the best support for importing tax data from employers (W-2 forms) and financial institutions (1099 forms for investment income). Its user interface is polished, its integrated access to a huge user community is a great resource, and Intuit includes free access to tax experts if you have a thorny question. Prices range from Basic ($35 online, $40 CD or download) to Home and Business ($100 online, $110 CD or download).

YARDENA ARARTurboTax’s interview-based user interface remains the most polished approach we’ve seen in a tax package.

The costs of preparing and e-filing a state return depend on which Intuit product you use. For any online version of TurboTax, state prep and e-filing together cost $40. If you purchase or download desktop software, the state e-filing costs $20 per state, with a maximum of three state filings per federal tax return. Buyers of a TurboTax Basic CD or download have the toughest deal: They must buy the separate TurboTax State package for $45 (it’s included in all other CD/download versions) and also pay $20 to e-file.

H&R Block offers free signoff from a tax pro

H&R Block, meanwhile, continues to use its huge network of tax professionals to chip away at TurboTax’s market leadership. Prices range from online consumer versions for $35 (Basic) to $75 (Premium), and downloadable versions from $30 (Basic) to $90 (Premium & Business). Yes, the Basic version is cheaper as a download than as an online service.

YARDENA ARARH&R Block’s Best of Both bundle includes review and sign-off by a tax pro.

Block differentiates itself from TurboTax with its $100 Best of Both offering. Best of Both lets you prepare your taxes online using the service’s Premium software, and then submit your return to a Block tax pro. This person will review your return for deductions and credits that you may have missed and will then sign off as your tax preparer. The Best of Both package also includes audit support, an extra-cost option with TurboTax.

TaxAct is the best budget choice

TaxAct continues to be a great deal for people who don’t need a deep dive into tax issues or access to a lot of tax-pro help. It offers a completely free federal return, e-file included. To file a state return, you must pay $18. For $2 more, you can get the same bundle with the Deluxe federal edition, which offers data import and other extras. Help with major “life events” is limited. This year, the free version covers hurricane damage and one other event.

YARDENA ARARTaxAct remains the most budget-friendly full-fledged tax package.

That’s still a bargain compared to just about all of the smaller Web-based tax prep services, and TaxAct has a pleasing user interface and some useful data-import options. It can import from the investment-tracking site GainsKeeper, for example. You do have to pay extra for some services that are free with other apps—for example, storing a previous year’s data.

Tax prep via smartphone or tablet remains limited

PC-based solutions remain the best option for most users, because tax-prep apps for tablets and smartphones are still scarce and pretty limited. Intuit’s pioneering SnapTaxbegan a couple of years ago as an iPhone app and is now available for Android devices (version 2.1 or later). With SnapTax, you photograph your W-2. The app includes OCR (optical character recognition) software that fills out tax forms using data it draws from the image.

INTUITIntuit’s SnapTax app supports iPhone and Android phones.

Not everyone can use SnapTax. One limitation is that you can have only W-2 forms, and interest or unemployment income not exceeding $100,000 ($120,000 if married and filing jointly). You also can’t claim a deduction for home mortgage interest. This year, for the first time, you can claim deductions for dependent children and daycare expenses. SnapTax costs $25 (covering federal and state e-filing).

H&R Block beats that with an iPhone/Android app that’s free—if you can file a 1040EZ form (meaning that you can’t claim dependents). It uses the same method as SnapTax, of camera-phone snapshots and OCR software of W-2 forms. You can e-file both federal and state returns for $10. Block does offer a few extra-cost in-app upgrades: For example, it charges a $5 smart-import fee for importing W-2 info (the OCR is for income values only).

TurboTax offers its full suite of tax software for the iPad, with the ability to store your data online for easy access. The iPad app incorporates the OCR capabilities in SnapTax so you can photograph your W-2. There’s no price advantage to using the iPad app.

H&R Block has an iPad app, too, but it just mimics the free, and very basic, Web-based version. It’s a free app with free e-filing for your federal return. State returns cost $28.

YARDENA ARARTaxAct has iPad and Android apps that integrate with its online software.

TaxAct has iPad and Android apps that integrate with its online software, so you can start your return in a desktop browser and pick it up on your tablet, or vice versa. But you can’t work on your return if your tablet isn’t connected to the Internet. The apps are free, and the online pricing applies.

The big players offer a smattering of apps tor checking on the status of a refund, too, but you can go straight to the source: The IRS has a Get Refund Status page that provides the latest information if you enter your taxpayer ID, your filing status, and the amount you’re expecting.

The better your data, the better your tax return

Switching tax-prep services can be tempting, but proceed with caution. You’ll want to look into a prospective new service’s support for importing last year’s return info—especially if items such as depreciation may affect your tax bill. Almost all vendors make it easy for returning customers to retrieve this information, and a growing number make switching to them easier by adding the ability to import a saved PDF.

One final piece of advice: No matter how capable your tax software or service may be, the job it does is only as good as the data you give it. Be sure to gather all of your financial records before you get started, and be prepared to spend time on data entry, especially if you’re counting on deductions to reduce your tax bill. Even if your software supports data import from personal-finance programs, you should review the results for accuracy. Tax software can do the math and bring deduction opportunities to your attention, but ultimately it’s up to you to deliver the numbers that it crunches.

Martin Shenkman for Financial-Planning.com writes: Trust investing never seems to get simpler. The combined impact of the fiscal cliff tax deal - increased marginal tax rates, the new Medicare tax on passive investment income and changing techniques for drafting and planning trusts - have changed the ground rules for many estate planning strategies.

For financial planners, the challenge of investing trust assets, planning for liquidity to fund distributions and identifying optimal asset location decisions is now probably greater than ever. To illustrate some of the new or different issues and challenges planners will face, let's use a simplified hypothetical: Jane Smith, 65, a widow with $8 million in assets. She is in the top income tax bracket and is subject to the new 3.8% Medicare tax on unearned net income.

Let's assume, also for simplicity's sake, that she has a 50/50 allocation to bonds and equities. Her assets might also be divided between various accounts in the following way:

* An IRA, designed to shelter income, holds $2 million of bonds.

* An irrevocable trust formed for her benefit by her parents holds $2 million in equities, with a goal of growing assets outside of her estate. * A grantor trust that Jane established in 2012 holds another $2 million of equities. (A grantor trust is a trust that is taxed to the settlor - that is, the person who set up and funds the trust.)

* In her own name, she holds another $2 million of bonds.

Is this really an optimal plan? What considerations might be relevant to the planning process under the new tax paradigm? What lessons can be learned for other investment or trust situations?

SHIFTING TRUST ASSETS

The trust set up by Jane needs to be reviewed carefully. Is Jane the only current beneficiary? Can distributions be made to Jane's heirs?

This could be particularly important. Under the new income tax paradigm, it might be possible to allocate more income-producing assets to the irrevocable trust and then distribute income out to Jane's heirs, who are in lower tax brackets.

This type of trust, commonly called a "sprinkling" or "spray" trust, can be an incredibly useful tool in the current environment. Making a distribution to a lower-bracket family member will pull the income with it, and could potentially let the family avoid the higher marginal income tax rates and 3.8% Medicare tax.

So perhaps favoring income-producing assets in this trust would provide the family an overall income tax savings. Advisors will also need to consider other complications, such as the "kiddie tax" and alternative minimum tax.

DECANTING OPTION

What if only Jane is listed in the trust as a current beneficiary and her heirs are beneficiaries on her death? In that case, the use of "decanting" might be helpful. This is the process of pouring an existing trust into a new trust to achieve desired legal or tax benefits. Decanting into a new trust that makes the heirs current beneficiaries would provide an income tax planning opportunity. Can that be accomplished? Will there be gift-tax or other adverse consequences from the decanting? The key point for planners is this: Don't assume that an irrevocable trust is what it is. If a trust is not optimally drafted, you may have options - perhaps including a decanting - and failing to pursue them may shortchange your client.

INCOME TAX CONSIDERATIONS

The recent round of tax changes also create another potentially thorny issue that planners should gear up to address. Suppose Jane's trust has all her descendants as heirs. Although there had been an income tax cost in prior years, the trustee may never have made a distribution - perhaps because of the potential estate tax savings from growing assets outside the transfer tax system, and maybe for personal reasons, as well.

Now, more than ever, trustees who limit distributions so that income is taxed to the trust may face challenges by beneficiaries. Bear in mind that trusts face a very compressed tax rate structure, so that a trust will bear the maximum income tax rate plus the 3.8% Medicare tax on about $12,000 of income. If beneficiaries are in lower brackets, they may demand distributions and justify the requests by the tax savings - in effect arguing, "I don't pay the Medicare tax, but the trust does. So give me the money."

That limited, self-serving perspective may not comport with the realities facing a trustee or advisor.

KEY FACTORS To make the decision, the trustee or advisor will need to consider the following factors: * The detailed terms of the trust. Bear in mind that a general reading of trust distribution provisions might have sufficed in prior years, but it may no longer be adequate to address these issues. Are distributions optional or mandatory? Is there language that suggests when and if distributions should be made? * The amount of income involved and the potential for tax savings. * Income tax status information on the beneficiaries, including federal tax bracket, adjusted gross income, state of residence and more. Not all fiduciaries, especially family trustees, have always gathered this information. It may now be even more advisable. And what happens if one beneficiary is in a much lower bracket than another? The real world complications may make this process quite daunting. * The Prudent Investor Act in the state whose laws govern the trust. The act lists a number of factors besides taxes to consider in determining a trust's investment policy. If a distribution is not being made, or investments that reduce income are favored, planners should be certain to document each relevant factor. * The trust's own investment policy statement, which should support the decisions made. Revisions to the policy statement may be required to address the new tax environment and the possibility that beneficiaries will demand distributions.

BYPASS TRUST ALLOCATIONS Traditionally, a typical estate plan involved the formation of a bypass trust and marital trust on the death of the first spouse. Once the death occurred, the bypass trust and marital trust would be funded. And generally, the bypass trust was weighted disproportionately with equities, in order to shift as much appreciation as possible outside the surviving spouse's estate. After the fiscal cliff tax deal, however, some clients will opt for outright bequests or marital trusts so that the assets bequeathed will be included in the taxable estate of the surviving spouse to receive a step-up in income tax basis on the second spouse's death. In contrast with past strategies, these clients will likely rely on portability to avoid federal estate tax on the death of the second spouse. Those opting for non-trust "simple" distribution plans will expose assets to creditors, remarriage and other risks that could prove more devastating than the estate or income tax. Many clients who live in states that have decoupled from the federal estate tax may opt for bypass trusts to reduce state estate taxes, even if they are never going to be subject to federal estate tax. Here's an example: Tom and Mary Johnson live in New York, which has an exemption of only $1 million. Their estate is worth $4 million total, so they will probably never have a federal estate tax. But on the second death, their heirs would face a New York estate tax on $3 million (the $4 million total less the $1 million exemption). Now if, upon the first death, $1 million was put in a bypass trust, they would reduce the ultimate New York estate tax by an additional $1million. But for those opting for a bypass trust, the issue is whether the state estate tax savings will outweigh the loss of the basis step-up. This is because the $1 million put in a bypass after the first spouse dies will be outside of the surviving spouse's taxable estate (which will help save on state estate tax) - but that also means no basis step-up on the survivor's death, so the heirs could face more capital gains cost.

INVESTMENT LOCATIONS What does all this mean to investment location decisions? In the past, it might have been best to pack equities into the bypass trust to maximize estate-tax savings. Under the new paradigm, however, it might make more sense to have 100% bonds invested in a bypass trust in order to limit the potential for growth. Putting equities in the marital trust (or in the surviving spouse's personal investment portfolio) should result in concentrating appreciation in the surviving spouse's estate, where those assets can qualify for a step-up in basis. This is the opposite of what was typically done in the past. The key is that - given the flurry of new tax changes - advisors must revisit past assumptions about investment planning and, in particular, asset location.

Over the past several years, most of the public discussion over tax policy has focused on how much the wealthy should pay and what the top marginal tax rate should be. After extensively debating the disincentive effects of raising the top marginal rate from 35 to 39.6 percent, Congress took that step in January. During the 2012 presidential campaign, the low average tax rate paid by Republican nominee Mitt Romney sparked much controversy as well. However, far less attention has been paid to marginal and average tax rates at other points in the income distribution. In many cases, low-income households face implicit marginal tax rates that far exceed those paid by high-income households. And economic research suggests that the decision of low-income individuals to enter the labor market depends on the average tax rate that they face.

This article discusses the role of both average and marginal tax rates throughout the income distribution. Our analysis relies on optimal tax theory, which allows us to study the trade-off between two of the main goals of policymakers: progressivity and economic efficiency. We briefly review the implications of standard optimal tax theory for setting the top tax rate, then turn to the trade-offs involved in setting the marginal tax rate at other points in the income distribution. We then extend the model to allow for individuals to enter and exit the labor force. Introducing an extensive margin of labor supply implies that average tax rates can play an important role in influencing work incentives. We next consider life cycle concerns. We conclude with a discussion of how understanding the tradeoffs involved in optimal taxation might inform policy decisions. We argue that a proportional tax system with a universal transfer or personal exemption provides a transparent tax code that deals well with many of the trade-offs involved in setting marginal and average tax rates. In making connections between optimal tax theory and current policy, we focus not just on the tax system but also on the system of transfer payments. Tax and transfer systems should be considered together because phasing out a transfer payment as an individual’s income increases is economically equivalent to taxing the additional income.

Selection of key findings:

Following extensive debate about the disincentive effects, Congress raised the marginal tax rate on the highest earners in January 2013.

But low-income households face effective marginal tax rates nearly the same as upper income households (30%), according to the Congressional Budget Office. Individuals face high implicit marginal tax rates at lower incomes because of the phase-out of government benefits, which is economically equivalent to taxing the income.

Similarly, secondary earners - usually married women -- face higher tax rates on their earnings because their entire income gets taxed at a rate that is at least equal to the primary earner's marginal tax rate.

Taxing income discourages work, thus these individuals are incentivized to stay out of the labor force.

Policy Recommendation:

A proportional tax system would improve transparency and efficiency by eliminating the variation in marginal and average tax rates within income groups. It could be made progressive by adding a universal transfer payment or an income exemption. CLICK HERE TO READ THE ENTIRE PAPER / ARTICLE

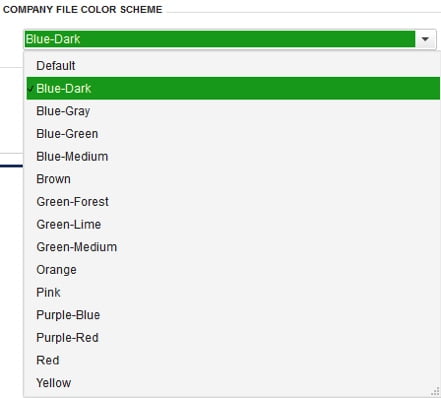

Woody Adams for RadioFreeQB.com writes: Hello Radio Free QuickBooks land, how goes it today? Are you using 2013? Do you want a more obvious way to color code a company file….to make sense of your multiple QB file universe? R6 has landed, as I am sure you have heard by now.

Last night I am watching a movie. I think Nick Cage is in it, called “Stolen”. For the most part entertaining, but I was really just biding my time, chomping, till the R6 webpatch hit the support site. I kept checking every 5 minutes or so as my buddy Jacint told me it would be there by 8:30 PST. But he just have been out surfing, cause the next thing I knew is it was morning and I was sleeping on top of my laptop…on the floor. No idea how I got there. Fortunately for me, Nic threw a blanket over me at some point during the night. As I was firing up the QuickBooks support site to download and install R6, I kept wondering what the hell happened to Nick Cage. I think he lived. Yup, he saved his daughter from some maniac and lived. I think he even faked out the cops and kept the gold, or at least 300 K worth. Nick doesn’t care about R6. His accountant uses QBO. You and I and all our desktop peers should care. Here is why…

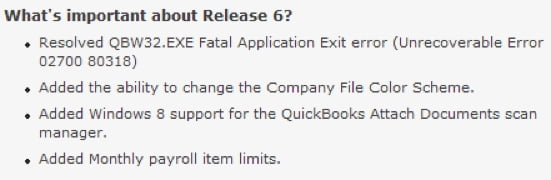

Other than solving for some of the known stability issues in QB 2013, R6 gives us more company file color options. You find these options where you would expect them to be, Edit/Preferences/My Preferences:

Once you select your color, here is what you will see. The color is wicked obvious (I am from the Boston area, though this word was not in the vernacular back in the 70’s), and the colors are at the top and outlining the windows. The default color is black. The left icon bar remains black regardless, but I know a lot of us are using the Top Icon bar. Remember, R5 gave us the ability to change the top icon bar to the older light blue coloring. There are some other minor UI changes for the better, one being form field names are in CAPS. To me, it looks crisper, and with the company file coloring outlining windows, I now like using the Left Icon bar as I like the color combination. It is fresh, sharp, elegant ( I never use this word….ever). He doesn’t. I can vouch for that. -Stacy

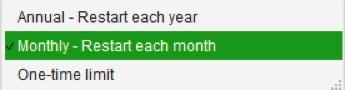

And for those who do payroll and have wanted to set item amount limits not just annually but by Month, that is in there too. Someone will care about that one…

Perusing the KB article above for R6 details, here are some changes I think are cool. This may or may not be relevant for everyone, but I am glad they got in there:

Banking

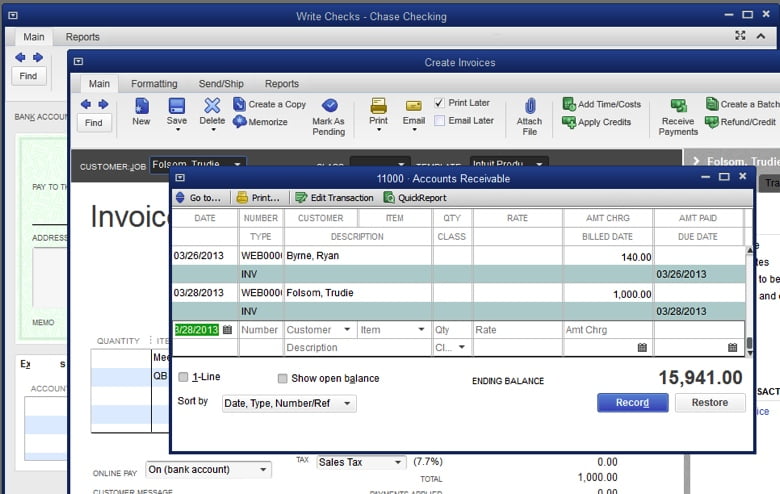

When the sort by option “Date,Type,Number/Ref” is chosen, deposits will now be listed first for transactions created on the same date.

Batch Enter Transactions

Batch Enter Transactions’ menu item is now accessible under the Company menu for non-accountant versions of QuickBooks Enterprise v13.0.

Centers

The Item Image window has been re-sized to support lower resolutions.

Increased the number of rows visible on the Bins tab in the Inventory Center.

All customer information (phone, email, etc.) will be added to any new jobs created for it.

Multi-currency

When multi-currency is enabled, total values will be reflected properly on a Purchase Order when it is created from an Estimate.

Payroll

Pressing the “s” key on the Employee Defaults window will act as a hot key to select a Class.

Improved performance of the Send Payroll Data workflow.

QuickBooks will not prompt to send Direct Deposit for Vendor payments if Direct Deposit for Vendor is not active for the company file.

QuickBooks will no longer display the message “You have Direct Deposit checks to send” when there are no checks to send.

Monthly payroll item limits are now supported.

After a check is voided and sent to Intuit using Direct Deposit, only a Cleared watermark will be displayed.

PDF

Improved overall PDF performance by resolving issues that prevented the ability to save as PDF.

QuickBooks Online Banking

QuickBooks will no longer display the error “There is Not Enough Memory to Complete this Action”, when attempting to deactivate an account set up for online banking.

QuickBooks Online Services

The Pay Online option on the Write Checks window will now be enabled in company files with multi-currency enabled and running in multi-user mode, only if the base currency is selected to USD.

Reports

Sales Description will now show on all reports except for Purchase reports

Resolved an issue that caused the word “Overflow” to show on a memorized cash basis custom transaction detail report instead of dollar amounts

R6 is a critical release for all desktop QB 2013 users, accountant and client alike. When you launch your QB Pro, Premier or Enterprise Solutions 2013 product and get the prompt to install the update, click Install Now.