The IRS has some advice for taxpayers who missed the tax filing deadline.

File as soon as possible. If you owe federal income tax, you should file and pay as soon as you can to minimize any penalty and interest charges. There is no penalty for filing a late return if you are due a refund.

Penalties and interest may be due. If you missed the April 15 deadline, you may have to pay penalties and interest. The IRS may charge penalties for late filing and for late payment. The law generally does not allow a waiver of interest charges. However, the IRS will consider a reduction of these penalties if you can show a reasonable cause for being late.

E-file is your best option. IRS e-file programs are available through Oct. 15. E-file is the easiest, safest and most accurate way to file. With e-file, you will receive confirmation that the IRS has received your tax return. If you e-file and are due a refund, the IRS will normally issue it within 21 days.

Free File is still available. Everyone can use IRS Free File. If your income is $57,000 or less, you qualify to e-file your return using free brand-name software. If you made more than $57,000 and are comfortable preparing your own tax return, use Free File Fillable Forms to e-file. This program uses the electronic versions of paper IRS forms. IRS Free File is available only through IRS.gov.

Pay as much as you can. If you owe tax but can’t pay it all at once, you should pay as much as you can when you file your tax return. Pay the remaining balance due as soon as possible to minimize penalties and interest charges.

Installment Agreements are available. If you need more time to pay your federal income taxes, you can request a payment agreement with the IRS. Apply online using the IRS Online Payment Agreement Application tool or file Form 9465, Installment Agreement Request.

Refunds may be waiting. If you’re due a refund, you should file as soon as possible to get it. Even if you are not required to file, you may be entitled to a refund. This could apply if you had taxes withheld from your wages, or you qualify for certain tax credits. If you don’t file your return within three years, you could forfeit your right to the refund.

Kimberly Lankford at Kiplinger's Personal Finance Magazine for MSN Money writes: This is the perfect time of year to go through your old files and shred financial records you no longer need. The IRS generally has up to three years after the tax-filing deadline to audit your return, so you can get rid of a lot of paperwork after April 15.

Don’t toss your tax returns (including your 1040 and supporting tax forms); you should keep them forever. They can provide important information in the future -- if, for example, you need to provide tax information when applying for a mortgage or getting disability insurance. You can keep the paper forms or digital copies.

But go ahead and ditch supporting documents three years after the tax-filing deadline. That includes credit-card statements, canceled checks or receipts to show deductions, letters from charities reporting gifts, and paperwork reporting mortgage interest or capital gains distributions. See IRS Publication 552 Recordkeeping for Individuals for more information about tax records.

And there are a lot of other financial documents you can toss (or, even better, shred) even sooner, if you don’t need them for taxes. You can get rid of monthly brokerage statements as soon as you check the numbers against your year-end statement, credit-card receipts as soon as everything matches up with your monthly statement (unless you need to keep them for tax purposes, such as documenting a business expense) and pay stubs after they match up with your annual pay reported on your W-2 (but save your December pay stub if it shows charitable contributions made by payroll deduction).

You can also dispose of copies of your utility, phone and cable bills as soon as the next month’s bill arrives reporting that your payment has been received (but keep utility bills with your tax records if you’re taking a home-office deduction or with your house records if you’d like to show prospective home buyers the cost of maintaining your house). You may not need to keep some files at all if they are easily accessible online -- utility, credit card and loan statements are generally available online for a year or more.

Hang on to a few tax-related documents more than three years:

Keep records of stock and mutual fund purchases made in taxable accounts for as long as you hold those investments. When you sell the stocks or funds, you’ll need to report the purchase price, date of purchase, and number of shares.

Keep Form 8606 reporting any nondeductible IRA contributions until you withdraw all the money from your IRA, so you won’t be taxed again on those contributions when you take out the money in retirement.

Keep home-purchase and home-improvement documents until three years after you sell the home. Most people no longer need to pay taxes on their home-sale profits – single filers can exclude $250,000 in profits, and married couples filing jointly can exclude $500,000, as long as they’ve lived in the home for at least two of the past five years. But if you haven’t lived in your house for that long -- or if your profits are larger than the exclusion -- then the home-improvement records can substantiate a boost in your tax basis (your investment in the house) and reduce any taxable gain. See IRS Publication 523 Selling Your Home for details.

Some people keep all of their tax records for up to six years if they’re self-employed, especially if they have income from a variety of sources. The IRS has up to six years to audit people who neglect to report more than 25% of their income.

Elizabeth Wine for Financial-Planning.com writes: Instead, encourage some of these clients to file for a tax refund -- now. Under current law, gay widows and widowers do not get any of the tax breaks their straight peers do, including the exclusion from paying estate tax. So clients who were legally married in the nine states that recognize gay marriage -- Connecticut, Iowa, Maine, Maryland, Massachusetts, New Hampshire, New York, Vermont, Washington -- plus the District of Columbia are on the hook to pay far more in taxes than if their late spouse were of the opposite sex.

In one of the same-sex marriage cases before the Supreme Court now, Edie Windsor is applying for a refund on the $363,053 she had to pay on the estate of her wife, Thea Spyer, because she was not granted the marital deduction on federal estate taxes.

'PROTECTIVE REFUND'

The paperwork clients should file is called a protective refund claim, and they should file it as soon as possible, said Philip T. Davies, an estate attorney in New York. “The law may be in some state of flux, but it's always better to file promptly (including corrective claims) based on your best rational and reasonable position, rather than wait for the law to be clarified,” he says. “Were we to wait forever there would have been no Boston Tea Party.”

He adds that there would be no negative repercussions for clients who file, even if the Supreme Court upholds the Defense of Marriage Act, the federal law forbidding gay marriage. “The worst case is simply the taxing authority rejects your claim, but even that outcome may take some time. Better an outright rejection of claim than having an uncertain claim you never filed.” The statute of limitations on tax refunds is ordinarily three years, says Matthew Erskine, an estate tax lawyer whose Worcester, Mass., firm also provides family office services. But gay and lesbian clients may get a break on timing; he notes that the IRS has extended filing windows in the past for “unusual circumstances,” and adds that a change in federal treatment of marriage could constitute such a circumstance. OTHER BENEFITS Depending on how the high court rules, married same-sex couples may also be able to take advantage of “numerous other federal tax provisions that provide benefits to married persons,” Florida tax attorney Charles Rubin has noted in his Rubin on Tax blog. Among the provisions that Rubin suggests cites: “(a) the federal gift tax marital deduction, (b) joint tax return filing rates and permissions, (c) favorable “stretch” and rollover provisions for IRAs and other qualified retirement plan distributions to a surviving spouse, and (d) portability of unified credit amounts between spouses."

Respect for Marriage Coalition for the Wall St. Journal writes: Leading voices in financial planning and diversity and inclusion share tips to navigate these economic inequalities. While many Americans dread April 15(th) , tax season comes with additional challenges and hurdles for married same-sex couples. CNBC Host Suze Orman and two Ernst & Young LLP leaders participated in a press conference call Monday to discuss the challenges same-sex married couples face during tax season and shared some financial planning tips. During this call, coordinated by the Respect for Marriage Coalition, Suze Orman discussed the financial challenges individuals face.

"In order to be financially secure now and in the future, same-sex couples have to devote time to financial and estate planning," said financial advisor and CNBC host Suze Orman. "DOMA requires families to look ahead and plan a budget around its restrictions, which includes higher federal taxes and tax penalties on benefits."

The patchwork of laws across states, counties, and cities in the United States pertaining to same-sex marriages -- along with DOMA -- leaves many couples facing different protocols, paperwork, and additional financial costs. Because of DOMA, married same-sex couples and their families are not federally eligible for -- and their spouses are not entitled to -- the same economic benefits and protections available to married straight spouses. Elda Di Re, Partner, Personal Financial Services Area Tax Leader, Ernst & Young LLP, discussed the challenges the company has seen as financial advisors, and also highlighted specific tips for same-sex couples on how to navigate the tax system.

"Many couples find filing taxes complicated as it is, but the differences between federal and state filing for same-sex couples make their situation even more complex," said Di Re. "It's important that couples know how to separate and file state and federal returns, make sure they're reporting their income and deductions properly, and plan ahead for potential action to end DOMA."

DOMA also presents challenges for businesses that offer competitive benefits for all employees. These benefits for married same-sex families are treated as taxable income, which the Center for American Progress estimates costs millions of dollars annually.

Karyn Twaronite, Americas Inclusiveness Officer for the global Ernst & Young organization and Ernst & Young LLP partner, addressed the business case for lesbian, gay, bisexual and transgender (LGBT) inclusiveness and what companies can do to help same-sex couples.

"The war for talent in the professional services sector is incredibly fierce, and attracting and retaining LGBT talent is critical to our success," said Twaronite. "As a starting point, companies can help LGBT couples facing inequalities by recognizing same-sex married couples the same way they recognize opposite-sex married couples in their processes and communications. Organizations can also make a difference through their own policies, such as offering a tax gross up to cover the extra tax same-sex couples pay on health and welfare benefits in the US. Additionally, companies can educate decision-makers about the inequities they witness but can't address, including same-sex couples losing tax savings since they can't put money into their health care reimbursement accounts for their partners."

DOMA hurts same-sex couples and families in many ways at tax time. Due to the complexity of tax law and the additional complications same-sex married couples face, the Respect for Marriage Coalition highly recommends that same-sex married couples hire an accountant or tax attorney to help navigate the tax process.

Regardless of which state a same-sex married couple lives, they must file their federal income tax as "single" for their federal taxes. In addition to not being able to file as "married," same-sex married couples must also pay a tax on any benefit an employer offers to the same-sex spouse of an employee. When a same-sex couple divorces, the alimony one spouse pays to another is not an allowable deduction as it is for a different-sex married couple. And for many families, they must take part in the painful process of dividing up the family and deciding which parent can claim their children on their tax forms. Mark Maxwell and Tim Young-Maxwell from North Carolina are all too familiar with these challenges. Despite being together for over two decades, the couple -- who married in January of this year in D.C. -- and their marriage are not recognized on the state or national level. As parents for their four adopted children, they are not both legally recognized as their parents because of DOMA. From the bigger costs, such as federal taxes on health care, and higher legal and accountant fees to higher gym memberships because they are not recognized as a couple or family, the financial hurdles affect their bottom line and their family of six.

"We pay twice as much for our accounting fees each year for him to navigate his way through filing our taxes," said Young. "Because of DOMA, we have to file our federal taxes as if we were single, which creates additional confusing steps that we wouldn't have to do if we were a heterosexual couple. And, because both our state and the federal government don't recognize our marriage, Mark and I have had to split up the family during tax season, which is heartbreaking." The financial burden same-sex married couples face can be staggering:

-- Employees who receive health insurance for a same-sex partner through

their employers pay an average of $1,069 dollars more in annual federal

taxes than their married co-workers.[1]

-- Couples can wind up paying thousands of dollars more in federal income

tax and filing-related expenses when they have to file separately.[2]

In a 2010 economic analysis of tax inequality facing gay couples, University of Massachusetts Amherst Professor M.V. Lee Badgett determined that the majority of married same-sex couples in Massachusetts would pay on average $2,325 less in federal taxes if they were permitted to file as a married couple.[3] The remaining same-sex couples in Massachusetts would see no change at all (11 percent), or a small change, averaging in taxes of $502.36 (23 percent). The financial benefits would also extend to the federal government. In fact, the Congressional Budget Office estimated in 2004 that recognition of gay marriage would help the budget's bottom line by $1 billion a year over 10 years.[4] For more information about DOMA, the economic impact of not recognizing same-sex married couples on the federal level, and the Respect for Marriage Coalition's work to advance the freedom to marry, visit RespectforMarriage.org. For an audio recording of today's press conference call, please email press@respectformarriage.org.

The Respect for Marriage Coalition is a partnership of more than 100 civil rights, faith, health, labor, business, legal, LGBT, student, and women's organizations working together to end the Defense of Marriage Act (DOMA) and grow support for the freedom to marry. The Coalition is co-chaired by Freedom to Marry and the Human Rights Campaign.

Tracy Bunner for the Standard Examiner writes: There are times when the only way to lower your tax liability is to have more taxes withheld from your paycheck or retirement. As children leave the home, your tax liability begins to increase. After a child turns 17, and it doesn’t matter what time of the year this happens, you no longer qualify for the Child Tax Credit of $1,000.

This affects the amount of taxes you will owe. Once the children leave the home or turn 19 and are not full-time students or they work, if they make more than the exemption amount ($3,900 for 2013), they cannot be claimed on the parent’s tax return. This can greatly affect the amount of taxes you will owe.

These are events that need to be planned for during the year. I have seen many incidences of this happening this tax season. Taxpayers are unprepared for their tax bill because they did not make adjustments to the withholdings from their paychecks. Even if your children still live with you and you support them, if they are 19 and not full-time students, the income factor comes into play. The child may not even need to file a tax return, but that does not mean you can claim the child on your return if the child earned more than the exemption amount.

Another area that causes your tax liability to increase is if your deductions fall below the standard deduction rate. Deductions taken on Schedule A such as medical bills (more than 10 percent of your Adjusted Gross Income for 2013), state taxes withheld or paid during the year, property taxes, mortgage interest and charitable donations must add up to more than the standard deductions. For 2013, they are $12,200 for married filing jointly, $8,950 for head of household; $6,100 for individual taxpayers; and $6,100 for married taxpayers filing separate.

If you add up the amounts for medical and your income is $50,000, these medical bills must be more than $5,000 to even begin to get a deduction for them. If they are under this amount, you do not need to track your expenses. However, let’s say for example you make $50,000 and your medical bills were $5,500. You medical deduction is $500. It is not $5,500. The first $5,000 does not count; only amounts over this will be deductible.

Let’s take another example. You are a single taxpayer and give $2,000 to your local church. Your other deductions such as medical, state taxes withheld, property taxes and mortgage interest all must add up to more than $6,100 to get the deduction for your donation to your church. If you are a renter, had little taken out of your paycheck or retirement for state withholdings, the standard deduction of $6,100 will more likely be the better option.

Another way to reduce your tax liability is to lower your taxable income by contributing to your employer’s 401k or other retirement plan. This lowers the amount of taxable income and keeps your money with you instead of having more withheld from your paycheck for taxes. Talk with a financial adviser to take advantage of this option to lower your taxable income.

Planning throughout the year for life-changing events can help lower your tax liability.

But before you close the books on 2012, spend a few minutes thinking about taxes for 2013. Lower- and middle-income Americans can plan for tax breaks temporarily preserved this year. High-income Americans will need a strategy to handle the increased taxes coming their way.

Perhaps the best tax news for 2013 is that rates will stay the same for most taxpayers. But you'll have to act fast to take advantage of several tax breaks slated to disappear in 2014. Unless Congress acts, this is the last year teachers will be able to deduct as much as $250 in their out-of-pocket expenses for classrooms.

Ditto for homeowners paying mortgage insurance and tax-payers age 70-1/2 and older who withdraw as much as $100,000 from their traditional individual retirement account to give to charity. Normally, with-drawals from a non-Roth IRA are included as taxable income. The American Opportunity Tax Credit, which allows families to deduct as much as $2,500 in tuition-related expenses, has been extended through 2017.

It's not so rosy for those with big medical bills. Instead of being able to deduct any of those expenses above 7.5 percent of their adjusted gross income (AGI), this year's threshold is 10 percent.

There's also a new $2,500 limit on flexible spending accounts, which employees use to pay health expenses with pretax dollars. But "a lot of people had been moving to HSAs [health savings accounts] anyway," says Mark Luscombe, principal analyst at CCH Tax & Accounting based in Riverwoods, Ill. "So the overall impact of this might not be as great as it once might have been."

For high-income taxpayers, the outlook is even more clouded – and not only by that new 39.6 percent tax bracket for those earning $400,000 or more a year. Even if their paychecks are smaller than that, many high-income Americans face a number of new taxes and limitations that will eat away at their income.

One of the most visible new taxes is a Medicare surcharge known as the Net Investment Income Tax. For individuals with a modified AGI above $200,000 (or $250,000 if married and filing jointly), Uncle Sam this year will begin assessing a 3.8 percent tax on what they earn above that. The tax can be assessed against wage income or on investment income (taxable interest and dividends, capital gains, royalties, etc.), whichever is smaller.

Then there's the Medicare payroll tax, which charges an extra 0.9 percent on wage income above the $200,000/$250,000 thresholds. These two taxes combine in different ways, as shown in this example from Fidelity Investments: If Paul and Ann make $330,000 in wages and $42,000 from their investments, their modified AGI is $372,000. That puts them $122,000 over the $250,000 threshold for the Medicare surcharge for married couples filing jointly. But because their investment income ($42,000) is less than that, they'll only owe 3.8 percent on $42,000, or $1,596. They'll also owe an extra 0.9 percent – the Medicare payroll tax – on wage income above $250,000. In this case, that works out to $80,000, triggering a tax of $720.

Couples wanting to reduce that $2,300 tax bite will have to come up with a tax strategy.

"There are quite a few things that have to be done for people in that category," says Rick Rodgers, a certified financial planner in Lancaster, Pa., and author of "The New Three-Legged Stool: A Tax-Efficient Approach to Retirement Planning." The strategy will depend on the level of a taxpayer's wage and investment income.

If the priority is reducing wage income, taxpayers should try to time when they receive income and bonuses and when they make charitable contributions, says Tim Barry, a tax principal at BlumShapiro, a regional accounting firm based in West Hartford, Conn. If the strategy is to reduce investment income, then taxpayers may want to engage in tax-loss harvesting (balancing out investment gains by selling other investments at a loss).

High-income Americans will take other hits in 2013. While the capital gains tax rate stays the same for low- and middle-income earners (0 and 15 percent, respectively), it jumps to 20 percent for individuals earning more than $400,000 ($450,000 for married filing jointly).

Another wrinkle: Deductions are phased out as income increases. The personal exemption generally allows taxpayers to reduce their taxable income by $3,900 for themselves, another $3,900 for a spouse, if applicable, and for each dependent child. But starting with individuals earning $250,000 ($300,000 for married filing jointly), the exemption begins to phase out. It disappears completely for couples earning $422,500. Those taxpayers also face reductions in popular itemized deductions, such as for mortgage interest and property taxes, although they never disappear completely.

The new code could well change how high-income taxpayers invest, says Mr. Barry of BlumShapiro. Municipal bonds may become much more popular among the wealthy because their tax-exempt income can help reduce the bite from federal taxes.

Ike Ikokwu for the HuffPo writes: It's been said the only two certainties in life are death and taxes. While I can't help you avoid physical death, I can help you avoid paying taxes at retirement. But first, we have to agree on where taxes are likely to be at your retirement....especially if you're a baby boomer. In a prior article I wrote for The Huffington Post called The Real Fiscal Cliff, you will see that the real fiscal cliff to be concerned with is not what happened January 1, 2013. It's the threat of significantly higher taxes in the future.

Some of the reasons higher taxes are an almost certainty for our future include our tax history which show an average tax rate of 60% since taxes were first introduced as a temporary tax in 1913. It also includes our massive debt load, the interest on our debt, our unfunded liabilities for entitlement programs, pension guarantees and the like, the amount of money we spent on stimulus plans, bailouts, and the countless numbers of wars we've financed on a credit card.

To get a sense for how bad tax rates could be in the future, the Congressional Budget Office projects that if "Social Security, Medicare and Medicaid go unchanged, the rate for the lowest tax bracket would increase from 10% to 25%; the tax rate on incomes in the current 25% bracket would have to be increased to 63%; and the tax rate for the "former" highest bracket of 35% would have to be raised to 88%." http://www.cbo.gov/publication/41694

So if you agree with me that taxes will be higher in the future, the next question is how do your beliefs line up with your actions? In other words, are you accumulating money in the right kinds of investments to prevent you from suffering from significantly higher taxes in the future? In meeting with hundreds of people planning for retirement, I am yet to meet with someone who is actually accumulating money in the right investments to avoid this ticking tax time bomb. From a tax perspective, there are only 3 types of investments or "tax buckets" that you can accumulate money in.

Taxable Bucket: This would include any investment that generates a 1099 each year requiring you to pay tax on the growth of that investment. CD's, Stocks, Bonds and Mutual Funds certainly fit the bill. Since these generate a tax bill for you annually, the question is why have them in the first place? The answer lies in the fact that they are generally very liquid and as such make for good emergency reserve funds. Having too much money in these accounts, can cause you to experience unnecessary wealth transfers in the amount of taxes you pay. So the goal is to only maintain an ideal balance in these accounts. For an emergency reserve fund, many financial experts agree you need about 6 months of living expenses. So, that would be the ideal balance we want to see in this bucket from a tax perspective.

Tax Deferred Bucket: This includes any investment where the growth isn't taxed currently, but rather deferred until some later point in time, like at retirement, where the distributions are taxed as ordinary income. Qualified Plans like IRAs, 401K's, SEP's, TSA's, 403b's are good examples. There are two primary goals in arriving at an ideal balance in this bucket. The first goal is to manage the growth of money in these accounts such that when you are forced to take distributions from the account at age 70.5, those distributions are only equal to what your projected tax deductions (probably just your standard deduction and personal exemption) will be at retirement. A 55 year old married couple in 2013, can take a standard deduction and personal exemptions that total $20,000. At 3% inflation, by age 70.5, the projected tax deductions from both of those items would be about $32,000, which would be the maximum amount we would want them to take as distributions so as to end up with ZERO in taxable income for the year. The second goal would be to limit contributions to these types of qualified plans to just enough to get the full company matching contribution. Why? Because it's the matching contribution that helps you pay future taxes which would probably be at higher rates than your funding years.

Tax-Free Bucket: These are investments with 2 characteristics. First, they are free from any federal, state or capital gains tax. Second, they don't cause your social security income to be taxed at retirement. Hence, the ideal balance in this bucket is really unlimited. Good candidates include ROTH 401K's, ROTH IRA's, ROTH Conversions, Non-Deductible IRA's that are converted to ROTH IRA's, and Life Insurance Retirement Plans (LIRP's).

The beauty of planning for a total income tax-free retirement, is when you accumulate and plan properly for a tax-free retirement, you could have diverse streams of income at retirement from:

• A Roth 401K which would be non-taxable • A ROTH IRA which would be non-taxable • A ROTH Conversion which would be non-taxable • A Traditional IRA or 401K with distributions equal to your tax deductions at retirement which would also be non-taxable • A Non-Deductible IRA converted to a ROTH IRA which would be non-taxable • A LIRP which would be non-taxable • Social Security which would be non-taxable by virtue of your other sources of income being non-taxable or under the provisional income limitations

While owning any number of these tax-free bucket candidates requires that you pay the tax today to do so, I think you would agree that income taxes, like mortgage rates, are at an all time low. Paying taxes today to avoid paying twice or three times that amount in the future is certainly a financially prudent thing to do. Apply these principles to help you win the money game and enjoy a totally income tax-free retirement!

Marc Bastow for investorplace.com writes: It’s April 15, tax day, and while a few of you might still be rushing to the post office, hopefully most of you have already finished with tax season, and without much hassle. Whatever your status, it’ll be all over by tomorrow. And while 2013 taxes might be the last thing you’ll want to think about on April 16, there’s a few things you’re better off remembering and taking care of sooner rather than later. Here are three examples:

Retirement Contributions

401k and traditional IRA plans are the best way to build up a nest egg because they have tax benefits designed to both encourage participation and accumulate money. Both programs allow you to put in money or other assets into an account (or accounts) that can grow tax-free until you take funds out. Just keep in mind they operate under different rules.

You can put up to $17,500 in a 401k plan during the year, and if you are 50 1/2 years old, you can put in an additional $5,500 “catch-up” for a maximum of $23,000. If your employer has a matching plan, even if it isn’t for 100% of your contribution, even better! The total contribution between you and your employer cannot exceed $51,000 or 100% of your earned income. Another benefit here is that the contributions are taken from your paycheck on a pre-tax basis, so you won’t have to pay payroll taxes on them.

Contributions to a traditional or Roth IRA are $5,500, but once again, if you are 50 or older, you can add an additional $1,000 for a total of $6,500. In certain circumstances, the contribution to a traditional IRA provides a direct tax deduction.

Retirement Distributions

Distributions from those retirement accounts are equally important in tax planning for the coming year. Whether you are simply old enough to have to take those distributions under current tax law, or if you need to borrow or take money out for any other reasons, you should understand the rules — and penalties.

You can start taking traditional and Roth IRA distributions penalty-free at age 59 1/2; distributions prior to age 59 1/2 are subject to a 10% penalty, with some exceptions allowed. Unless you fall into these exceptions, it’s best to plan on not taking money out of a traditional IRA.

The IRS requires you to take IRA distributions by the April following the calendar year you turn 70 1/2, then every year thereafter, on or before December of that year. If you don’t take the minimum required distribution, you may owe an excise tax on a portion of the required distribution. And note, these RMDs are taxed as ordinary income for the tax year in which you take them.

Since Roth IRAs are taxed when you make contributions, distributions are treated somewhat differently, primarily depending on several factors, including when the withdrawal is made and for what purpose. “Normal” withdrawals that fall under any of these four rules are not subject to taxation:

Made on or after the date you become age 59 1/2;

Made to your beneficiary, or to your estate, after you die;

Made to you after you become disabled within the definition of the IRS code;

Used to pay for qualified first-time homebuyer expenses.

With regard to your 401k plan, any distributions are taxed as ordinary income.

Estate Tax Planning

If there was ever a complicated area for retirement tax planning, this one might win the gold medal.

While you definitely should hire a tax or financial planner to help on this front, there’s one easy action you can take to minimize your estate value — thus reducing the taxable estate for heirs — while doing something nice for someone … in fact, anyone.

The Internal Revenue Service annual exclusion for gifts now stands at $14,000 from any one individual without having to worry about a gift tax. Parents can combine their gifting so that any individual — say, a child — can receive up to $28,000 tax-free and without counting toward your individual $5.12 million lifetime gift-tax exclusion.

Stan Haithcock for MarketWatch writes: Annuities are growing in popularity every year with an estimated $200 billion to be sold in 2013. As with every investment, you have to consider the tax ramifications and should always receive all of your tax advice concerning annuities from a qualified tax professional.

The best overall resource I have found is a recent book by renown annuity tax guru John Olsen, called "Taxation and Suitability of Annuities." As John puts it so simply in his book, with annuities you have to prepare for taxes during life and after you pass away. Things get a little complicated when using annuities with Trusts and in estate planning, so this is further reason to always use a tax pro.

Below are some basic points to be aware of when it comes to commercial annuities. This list is by no means "all inclusive" and just scratches the surface on all the rules and exceptions, but is a good foundation if you currently own an annuity or are considering the purchase of one.

Tax deferral

Over 80% of all annuities are deferred annuities. With non-IRA money, you can place your money within a deferred annuity structure and not be required to pay taxes until money is taken out. All gains grown and compound tax free during the deferral years. When you eventually take money out, it is typically taxed at ordinary income levels and using LIFO (last in, first out) accounting.

Annuity payments

Annuities were developed to pay an income stream for life, regardless of how long you live. The two ways you can receive a lifetime income stream from an annuity is by annuitization or drawdown.

Annuitization — This is the original way to create a lifetime income stream. With non-IRA funds, annuitization provides an income stream of which a portion is excluded from taxes. This is called the “exclusion ratio.” Annuitization is a combination of return of principal and interest, and all deferred annuities can be annuitized for income needs.

Drawdown — The newest way to create a lifetime income stream with deferred annuities. This strategy is primarily used with the now popular “income riders” which are attached benefits to a policy that can be used for lifetime income. Using non-IRA funds, the income stream is taxed at ordinary income levels and using LIFO (last in, first out). LIFO taxation applies if your annuity was purchased after Aug. 13, 1982 and no additions were made after that date.

1035 transfer rule

The IRS approved 1035 transfer rule allows you to transfer a non-IRA annuity to another non-IRA annuity without triggering any taxes. Whatever your cost basis is with your initial annuity will transfer to the receiving annuity company. You will eventually have to pay taxes when you take money out of the annuity.

Taking money out

The majority of deferred annuity contracts allow you to take money out on an annual basis if needed.

10% free withdrawal — Deferred annuities allow you to take out money from your annuity on an annual bases without incurring surrender charge penalties. Most policies allow 10% of the accumulation value to be withdrawn, and the taxation is LIFO if there are gains in the policy.

59 ½ Rule — Just like with your IRA, if you take money out of a non-IRA annuity, you will be penalized under the IRS early withdrawal rules. However, there is a way around this penalty utilizing Rule 72(t), if you really do need to access the funds earlier than planned. There are a few exceptions, like being disabled, that will not trigger the penalty.

Individual retirement accounts

Some practitioners don't believe in placing annuities within IRA's, and that is an argument for a different day. Right or wrong, hundreds of millions of annuity dollars are currently in traditional IRA's. Roth IRA's can house annuities as well, but the points below are for traditional IRA's.

IRA Transfer Rule — If you have a deferred annuity within an IRA, you can transfer that annuity directly to another IRA as a non taxable event.

RMDs — Annuities within an IRA that pay a lifetime income stream (like Immediate Annuities), can help cover your annual Required Minimum Distributions. The income stream from the annuity has no tax advantages within the IRA, and the income is taxed at ordinary income levels just like any money that you take out of your IRA.

Annuity death benefit

Annuities are life insurance products issued by life insurance carriers. However, unlike life insurance, annuities are taxable at death. Within an IRA, an annuity is taxed like other IRA assets. Outside of an IRA, the gains are taxed.

Stretch IRA — One strategy that will limit taxes at death is stretching your IRA using an annuity strategy. You can stretch your IRA without using an annuity, but fixed annuities provide a principal protected way to maximize this strategy. Stretching means that the spouse and subsequent beneficiaries can take the deceased IRA owner’s RMD’s over their life expectancy instead of paying taxes on the lump sum. This would permit them to only pay taxes on the RMD amount, and is a great legacy strategy as well.

With Washington in need over continually increasing revenue, expect annuities to be targeted as a new tax resource.

California, Nevada, and a few other states have already instituted a "premium tax" on annuity income and expect this trend to flow from the West Coast very quickly. I also predict similar new progressive taxes on annuities in the coming years.

Don't try to "do it yourself" when it comes to taxes on annuities. Always consult with a qualified tax professional.

Now that you have this year's taxes out of the way, it's time to get a jump on April 15, 2014.

1. Keep personal information organized.

Were you scrambling to find your kid's Social Security number? Did you forget your spouse's birth date? Tracking down this information just adds more time to an already time-consuming process. Pick a safe spot to store all the info you need. Consider a fireproof and waterproof safe that's large enough to store important letter-sized documents.

What to store:

Last year's taxes. You're going to want this year's tax returns to use as a guide for next year's, so keep them in a secure spot. If your life doesn't undergo major changes this year, filing taxes will be a breeze.

Personal data. Keep a list of important information like Social Security numbers and birth dates for you and your family.

Receipts. Start a receipt folder to store anything you might be able to deduct at the end of the year, such as home improvement purchases or business supplies.

2. Go digital. If you'd rather go paperless, there are apps for that likeDocVault. It lets you save 3GB worth of encrypted pictures and tax-related material like receipts and invoices, and allows you to add notes and tags to the photos for easy organization on DocVault's servers. Come tax time, you have the option of transferring those images directly to filing services TaxAct Deluxe or TaxAct Preparer's Enterprise.

Receipt Catcher is an app that lets you take a photo of a receipt, tag it with info, and then email it to yourself. When you're ready, you can print out a year's worth of receipts in a few clicks. The app costs 99 cents and is available for both Android and iPhone.

3. Start thinking about tax breaks.

Before you file those papers away, review which deductions and credits you qualified for in 2012 and determine which ones you'll be able to use this year. For example:

Home renovations. If you're planning some home improvements, check out EnergyStar.gov's list of products that qualify for a tax credit.

Home office deductions. I work at home, so I take advantage of all the deductions I'm allowed. Double-check and make sure your home office meets the IRS' requirements. Filing a Schedule C makes you 10 times more likely to get audited. Now is a good time to check this IRS fact sheet on what you can and can't deduct if you plan to upgrade your office.

Use your 2012 return to spot where you can and should save more money this year. For example:

Mortgage rates. If you haven't already, maybe you should consider refinancing to a lower interest rate.

Retirement savings. If you haven't put any money away for retirement, start now, even if it's just $40 a month.

5. Don't withhold too much.

Uncle Sam loves getting interest-free loans, and many taxpayers make it possible by overpaying their taxes. Last year, the average tax refund was $2,803. But there are ways to keep that money in your pocket. We have tips, like using the IRS' withholding calculator.

Take a few minutes to research what changes are in store for this year. Will the deductions and credits you used for 2012 be around for 2013? Are new deductions available? The more you know now, the easier it will be to minimize your tax liability.

Kurt Badenhausen for Forbes writes: Tax Day is upon us once again, where procrastinators stressfully rush through their returns to get them to the post office before closing time. The tax code is so convoluted that many people struggle through the ins and outs on which form to report income, which schedules to deduct expenses or even which items of income are taxable and which expenses are deductible. The tax returns for most people are relatively simple as compared to an athlete’s because they only have to know the rules for one state.

Athletes file taxes not only in their home state but also in every state—and some cities—in which they play. Not every state uses the same calculation to determine what portion of an athlete’s income to tax, and some use different calculations based on the sport. For example, Pennsylvania taxes baseball, basketball and hockey players on the ratio games in the state over total games played, including pre- and postseason, but they tax football players based on days worked in the state over total days worked.Michigan uses the same method but excludes the preseason. Most other states use the days worked method.

Reciprocity agreements can save an athlete thousands if their tax professional knows what to look for. For example, a Pennsylvania resident whose tax rate is 3.07% is exempt from paying taxes on money earned in New Jersey (8.97% tax rate),West Virginia (6.5%), Ohio (5.925%), Maryland(5.75%), Virginia (5.75%) and Indiana (3.4%). Because players come from all over and move around so much an athlete’s team will often times report income and withhold taxes in every state he plays, regardless of whether a reciprocity agreement with his home state is in place.

Taxpayers generally receive credits for taxes paid in other states. Usually, credits are taken on a taxpayer’s home-state return. But residents ofArizona, Indiana, Oregon and Virginia must take credits for taxes paid to California on their California return. Most of time, states will not give credits for taxes paid to cities. However, New Jersey gives people who work in Philadelphia and pay its 3.4985% nonresident wage tax a credit on their New Jersey return.

Unlike most of us, athletes can receive millions in signing bonuses. These bonuses are exempt from most states’ taxes if they are paid separately from salary, non-refundable and also not contingent upon playing for the team. So if Mario Williams’ contract was written properly, the Texas resident would not have to pay a dime in taxes to New York (or any other state) on the $19 million signing bonus he received when he signed with the Bills last summer, a tax savings of $1.676 million. It is a safe bet that Buffalo’s payroll department allocated the bonus to New York and the other states in which the Bills played. It is up to his tax advisor to catch it and make the necessary adjustment.

Finally, athletes get docked with hidden taxes in various jurisdictions. Tennessee hits basketball and hockey players with a $2,500 per game tax (max 3 games per year). Pittsburgh gets athletes for 3% of their wages for games played there. Although deductible on Schedule A of the federal return, neither of these taxes shows up on the player’s W-2. The tax preparer needs to have the player’s year-end paystub, where those and other deductions are often found. Many teams also mistakenly withhold Pittsburgh’s 1% wage tax. This tax is only imposed on Pittsburgh residents, so a refund request must be filed with the city to reclaim that money.

Yardena Arar for PC World writes: There's a reason QuickBooks remains the most popular small business accounting software. Intuit has spent 13 years honing its features, after all. Because there's a new version every year, however, you might not be up to speed on everything you can do to make QuickBooks easier and faster to use.

Whether you're building reports or seeking shortcuts to summon key information, these tips will save you time and keystrokes. Each tip is labeled with the QuickBooks edition year in which it first appeared, going back to QuickBooks 2010. Anything older is simply shown as pre-2010.

Make QuickBooks follow your preferences

QuickBooks offers a huge number of options in its Preferences window, which you access from the Edit menu. For each Preference item, you get tabs for personal and company options. The personal options apply only to the current user, while company options appear to all users. It’s worth clicking on both tabs to see all of your customization choices.

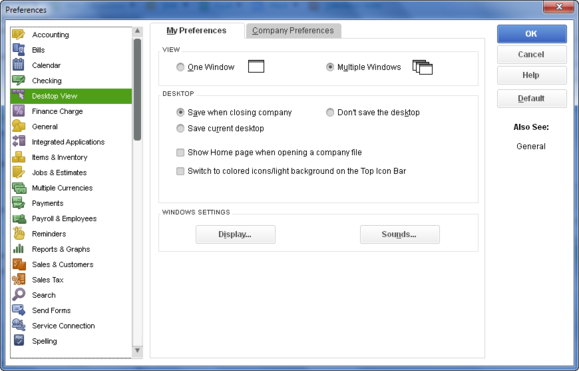

1. Choose your desktop (QB2010)

Desktop view

The default flow chart that appears when you first fire up a new copy of QuickBooks looks like something from an accounting class, but fortunately you’re not stuck with it. InPreferences, Desktop View you can opt for another startup screen, such as the popularCompany Snapshot, by going to the window you’d prefer and then clicking the Save current desktop radio button. Alternatively, you can have QuickBooks simply save the windows you’re working in when you shut it down by clicking Savewhen closing the company. In this same window, you can also choose between either the default option, keeping multiple windows open when you work, or the only one at a time option (when you open a window, the previous one automatically closes).

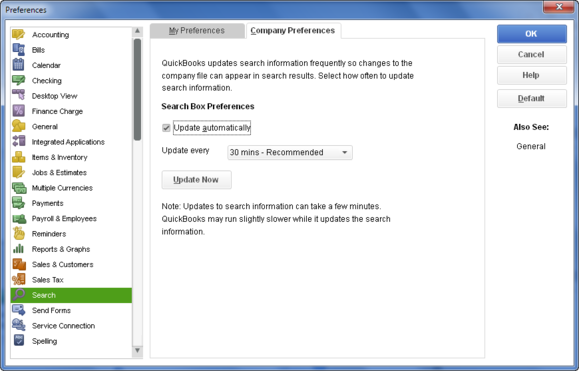

2. Speed up searches (QB2012)

Search

QuickBooks' search feature lets you find items in either your company file or the program’s help files. By default, a search field appears in the top icon bar (summoned in View, then the Top icon bar), but under Preferences, Searchyou can remove it, and also specify whether you want a company or help file search. (By default, QuickBooks lets you choose from a drop-down menu below the search filed every time you initiate a search.) In the Company tab, you can also specify how often QuickBooks should index your company file so that searches will reflect recent entries. QuickBooks recommends indexing at 30-minute intervals, but since indexing can slow down the program, you might want to opt for longer stretches. When you do need to find a recent transaction, you can always click the Update Now button in this window.

3. Find old messages (pre QB2010)

QuickBooks by default has a bunch of reminders that you can turn off by checking a do-not-show-this-message-again box in the message. But if you want to bring them back, just hop to the General preferences window and click the “Bring back all one time messages” box. Here you can also have QuickBooks use the Enter key to tab between fields, show (or suppress) clipped text in ToolTips, choose between using today’s date and the date of the last transaction for new transactions, and much more. The 2012 and later versions give you the option of running QuickBooks in the background in order to speed up its launch.

Work better with data and reports

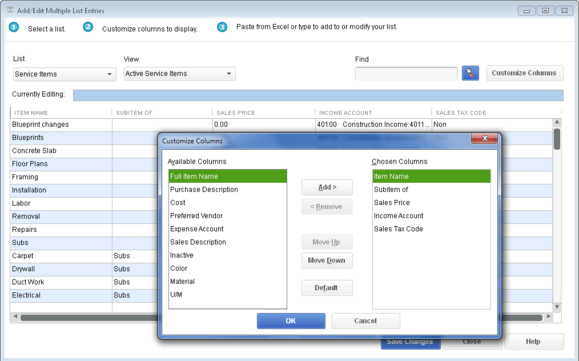

4. Add or edit multiple list entries (QB2011)

Multiple list entries

Say you need to update a QuickBooks list, anything from customers and vendors to services and parts. The Add/Edit Multiple Entries under the Lists menu item provides several handy ways to do so. By displaying list data in a spreadsheet-like grid format, it allows you to insert, remove or move around columns and paste copied Excel cells, in addition to simply typing in new entries. A Copy Down command that appears when you right-click a cell will fill out the rest of the column with the contents of the cell. However, use carefully as it will overwrite any previous contents.

5. Modify a report before it runs (pre QB2010)

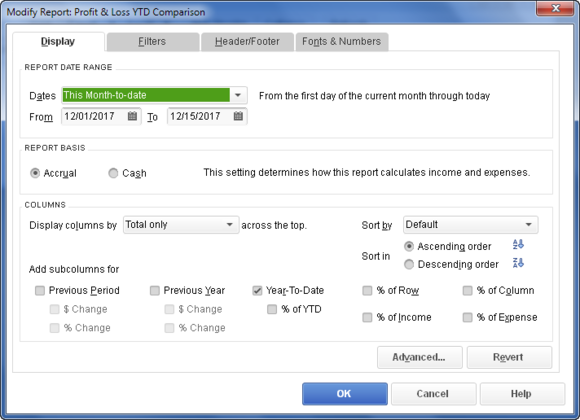

Modify a report

QuickBooks makes tweaking reports super easy, but you don’t have to wait for the report to open before making changes. Go to Preferences, Reports, and check off Prompt me to modify report options before opening a report. From then on, when you choose a report, you’ll get a window with its options before you run the actual report. If your data sets are large, this can be a real time saver.

6. Auto-refresh reports in Excel (QB2012)

Update reports automatically.

Many QuickBooks users like to export report data to an Excel spreadsheet, where they can make tweaks ranging from format changes to adding formulas. QuickBooks some time ago made creating the spreadsheet easy by putting an Excel button at the top of reports, which brings up a window with exporting options. You can even set some Excel options before exporting the data by clicking the Advanced button.

The problem with this in earlier editions is that refreshing the tweaked spreadsheet with new data from QuickBooks could be messy. Formatting changes, for example, were not applied to the new data. The 2012 edition of QuickBooks upgraded the Excel export functionality to address at least some of these issues. Once you’ve created an Excel workbook with exported data, QuickBooks creates a menu item in Excel that lets you update the spreadsheet without even running QuickBooks.

The process still isn’t perfect: QuickBooks even adds a sheet in Excel workbooks created using the export feature to explain some of its limitations. However, it can make life easier if you like to massage QuickBooks data in Excel.

Find shortcuts and menu customizations

7. Play favorites (QB2011)

QuickBooks has so many standard reports that finding the ones you use regularly from its menus can get annoying. You can avoid menu surfing by designating reports as faves by clicking on the heart icon underneath any report—standard, memorized, or contributed—in the Report Center. After that, it will show up in the Favorites tab in the Report Center, and there’s even a Run favorite reports command for getting all those reports to update with a single click.

8. Customize the icon bar (pre QB2010)

Don't just take the icon bar as it comes!

The standard QuickBooks interface is loaded up with icons to items you may never need, and sometimes the ones you want are missing. You can make the icon bar more relevant to the way you use QuickBooks by adding or removing icons in the Customize icon bar window by choosing View, then the Customize icon bar. Or, create new icons by clicking the Advancedbutton in that window.

9. QuickBooks product info (pre QB2010)

The QuickBooks product information window provides a wealth of statistics and other details you may need for tech support or other issues. Among other things, you can find out when you installed your copy, the exact release number, license information, details about the number of users and list items, and much more. Access it by pressing the F2 key on your Windows PC.

10. Pop-up calculator (pre QB2010)

Pop-up calculator

If you need to do some quick math on the fly while creating an estimate, a sales order or an invoice, there’s no need to exit the QuickBooks form. With your cursor on any dollar amount field, simply click one of the +, -, * or / keys (for addition, subtraction, multiplication or division), and a tiny calculator window will appear.

11. Lots of keyboard shortcuts (pre QB2010): People who prefer keyboard shortcuts to clicking around graphical menus and windows have lots of options in QuickBooks, many dating back to its DOS origins. For example, CTRL-F summons the detailed Find window for tracking down specific transactions; CTRL-R produces the register associated with the current transaction. There are also tons of context-sensitive shortcuts that only apply for specific data types—for example, if you’re working in a date field, hitting Y changes the date to the first day of the current year. To see complete lists of keyboard shortcuts, start by going to the QuickBooks help page on this topic. From there, you can access lists for all shortcut categories: General, Dates, Editing, Help Windows, Activities, and Moving Around a Window.