One general trend I saw this tax season was, as more and more median incomes rose shifting people into the next higher tax bracket, more often than not, retirement savings schemes such as the 401(k), the Individual Retirement Account (aka IRA) seemed to be the salaried man’s (or woman’s) major or only avenue to tax savings. This is what I tell my clients, if the government gives you an opportunity to avoid income taxes, you should graba hold of it and not let go.

There are various employer offered retirement plans, like the Section 401(k), 403 (b) etc. These have more or less the same rules for 2014. The maximum annual contribution for these plans remains unchanged at $17,500 and $23,000 if aged 50 and above. The Individual Retirement Accounts contribution limits also remain unchanged for 2014- $5,500 and $6,500 for age 50 and above.

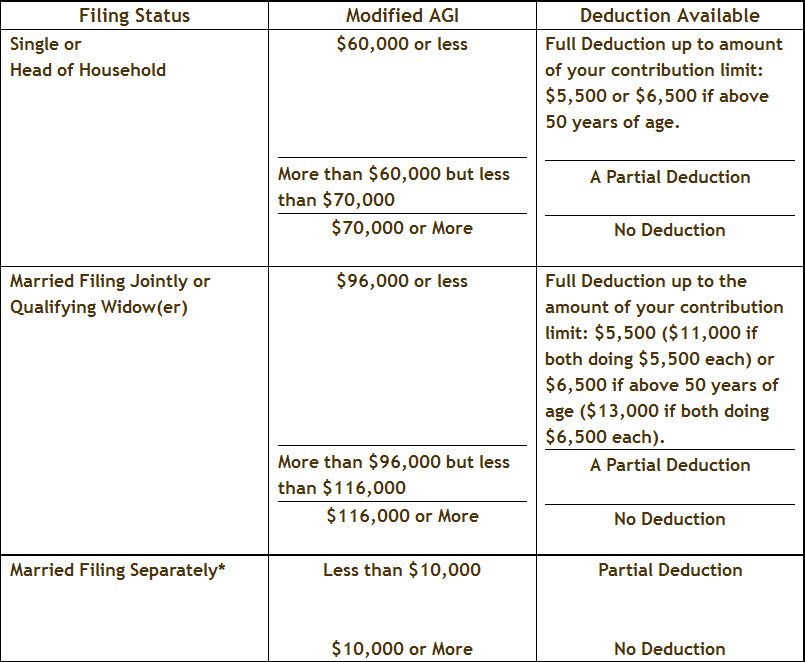

The maximum contribution limits are easy to remember. The tricky part is understanding the phase-out limits for tax deductions when contributing to an Individual Retirement Account.

Most of the confusion arises when taxpayers are already contributing into an employer retirement plan and want to bolster that with an IRA contribution. The table below should help:

*If filing with the MFS status and the taxpayer did not live with the spouse at any time during the year, the IRA deduction is determined as if under the “Single” filing status.

If you go through the above table you will get that being in the “Full Deduction” and “No Deduction” group is easy to figure out, however if you fall into the “Partial Deduction”, make sure you talk to a tax professional BEFORE you make your IRA contribution for the year.

I would say DO NOT try any of these calculations on your own if you do not know what your Modified AGI or MAGI is going to be for the year.

0 comments:

Post a Comment